Carousel Fraud: Why It Remains One of the Costliest Crimes

Ketan Karia – VP, Analytics EMEA

Carousel fraud, also known as Missing Trader Intra Community (MTIC) fraud, is one of the most sophisticated and damaging forms of VAT/GST evasion. Despite decades of enforcement efforts, it continues to cost governments tens of billions each year- and is the largest source of tax loss globally. Understanding why this fraud persists, and why it is so difficult to eliminate, is essential for designing effective countermeasures.

What is Carousel Fraud?

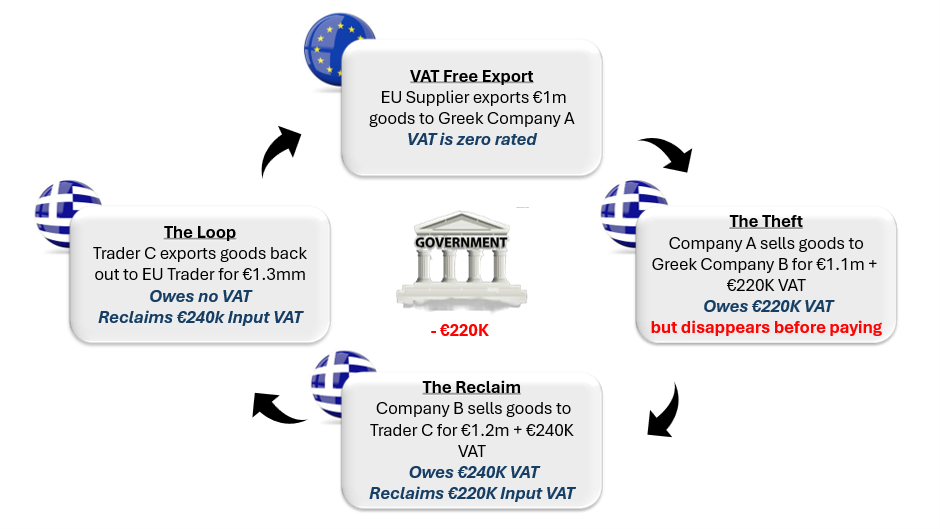

At its core, carousel fraud exploits the VAT system’s treatment of cross border trade. In many jurisdictions, goods traded between countries within a customs union or free trade area are zero rated for VAT purposes. This means businesses can purchase goods VAT free, then sell them domestically while charging VAT. The fraud occurs when the seller — known as the “missing trader” — collects VAT from the buyer but disappears before remitting it to the tax authority.

The scheme becomes a “carousel” when the same goods are repeatedly traded across borders through a chain of companies, generating multiple fraudulent VAT claims. Often, the goods involved are high value, easily transportable items such as electronics, precious metals, or carbon credits. In some cases, the goods may not even physically move; only the paperwork does

Why is Carousel Fraud so difficult to combat?

Despite regulatory and compliance efforts by authorities world -wide the fraud persists driven by the high returns. Fraudsters are coming up with new innovative ways to stay ahead of forensic teams and preventative legislation. The key obstacles to prevention remain as follows

Exploiting VAT cross border tax structures: In most countries worldwide, VAT treatment of exports is governed by the Destination Principle which generally means they are zero rated, while imports attract the prevailing local VAT rate. This preserves tax neutrality with the tax liability on the final consumer while the intermediaries claim VAT input credit. This globally accepted structure makes its exploitation difficult to eliminate without major tax reform.

Highly Organised Cartels: The anonymity and potential size of thefts attract international syndicates who are well funded, highly organised and nimble. Fraudsters create elaborate networks of shell companies, fake invoices, brokers, and intermediaries to obscure the flow of goods and money. These chains often involve legitimate businesses as buffers in the carousel to mask the fraud as normal trade to prevent detection.

Speed and Complexity: These networks, structures and schemes can be set up and dismantled quickly, making it hard for authorities to track them in real time. By the time forensic police become aware of a crime an begin an investigation, the companies involved have dissolved or faded into anonymity. Carousel fraud exploits weaknesses in traditional audit based enforcement. Audits are retrospective and resource intensive, while fraud networks operate rapidly and adaptively. Without real time data, tax authorities often detect fraud only after significant losses have occurred.

Communication Lethargy: By its very nature, carousel fraud is international in nature and therefore relies on cross border transactions. Effective enforcement requires cooperation between multiple tax authorities which simply does not exist uniformly across trade routes. Differences in reporting systems, data formats, and legal frameworks can slow down information sharing, giving fraudsters a significant advantage. Even when countries introduce digital sharing of export information, cartels respond by adding non-participating layers in their chain preventing AI driven automated systems flagging the fraud.

The Impact of Carousel Fraud

Vat Evasion causes significant challenges to economies worldwide with consequences impacting governments, businesses and citizens alike. The intricate web of financial implications has multiple dimensions that are explored below

Enormous Economic Loss: The scale of the financial impact on economies worldwide runs into hundreds of billions. The European Commission estimates their VAT Gap to be €128Bn while the US estimates their revenue shortfall to be $311Bn. In both cases evasion and fraud are the largest contributors to non-compliance. The shortfall impacts essential public services like healthcare, education, infrastructure and social welfare.

Market Distortion: Because fraudsters aren't paying taxes, they can sell high-value goods (like mobile phones or computer chips) on cross border eCommerce marketplaces at prices below market value, thus creating an uneven playing field that impacts honest businesses, stifles competition and undermines trust.

Victimising honest businesses: Because fraudsters often interpose legitimate companies in the supply chain to mask their activity, the honest companies are often badly impacted by a court ruling known as the Kittel Principle, where a business can be held liable for unpaid VAT in its supply chain if it "knew or should have known" about the fraud. This leads legitimate companies to suffer from sudden denied VAT refunds, causing severe cash flow issues. Clearing their name often involves long-running, expensive legal battles and irreparable reputational damage.

Criminal Financing: The high profits and relatively low risk of prosecution attract sophisticated organised cartels who then use the proceeds to fund their other criminal activities like drug and human trafficking, terrorism, cybercrime, violent robberies and other underworld illegal financing – leading to a compounded impact on the victimised countries.

Technology Led Fight Back

Despite these challenges, some countries have made progress using advances in AI powered Analytics to detect, prevent and prosecute VAT evasion across borders. The mechanisms used by the majority of OEDC members are documented in my previous blog VAT Fraud – The global cat and mouse game. They include real-time VAT reporting, e-invoicing, cross border data sharing, AI powered analytics, transaction monitoring, network analysis. Together they are designed to flag abnormal trading patterns and anomalies.

A real-life example code named The Admiral by the European Public Prosecutors is the largest VAT carousel fraud uncovered in the EU. The Baltic based syndicate used a complex network of over 400 companies across 15 EU countries syphoning in excess of €3 Billion over 8 years. While several individuals have been prosecuted, investigations continue as the case has uncovered links to drug trafficking, cybercrime and investment fraud.

These advances have helped authorities transition their enforcement efforts from manual and reactive to proactive real-time threat detection and prevention. It has levelled the playing field for the embattled enforcers who for so many years were outnumbered and outclassed by their better funded adversaries.

Some final thoughts

Ultimately, carousel fraud persists because it is highly profitable, difficult to detect, and relatively low risk for perpetrators. To combat it effectively, tax administrations must embrace modern technology, strengthen international cooperation, and adopt proactive, data driven enforcement strategies.

Carousel fraud is not just a tax issue; it’s a systemic vulnerability. Until tax systems evolve to close structural loopholes and detection becomes truly real-time, this “old” fraud will continue to reinvent itself and remain one of the costliest crimes in the modern economy.

Ready to see how the battle is being won?

Read our follow-up piece to see the tech in action: VAT Fraud – The Global Cat and Mouse Game.

Is your current infrastructure keeping pace with organized fraud? > Don't fight tomorrow's cartels with yesterday's systems. Contact us provides the speed and scalability needed to unmask "missing traders" in real time.

Ketan Karia – VP, Analytics EMEA

- Share on